Authorization and capture

Authorize and capture a payin in a two-step process with Rainforest

Feature requirements🔐 Rainforest must enable the platform to access this feature

💲 Billing fees associated to this feature

⬆️ Only available on the API version 2024-10-16

Rainforest supports processing Card payins with a two-step process to authorize the payin and then later capture the payin. This payment flow differs from the default payment processing that completes the authorization and capture in a single step.

Authorization will confirm there are sufficient funds on the user's credit card and place a hold on the funds. The payin will appear as pending on the user's credit card until the funds are later captured. In the Rainforest ecosystem, the payin will have a status of Authorized.

Capturing the funds will initiate the movement of funds from the user's issuing bank to the merchant. Once the funds are captured, the payin will appear as posted on the user's credit card. In the Rainforest ecosystem, the payin must be in the status of Authorized to be captured, and if the capture is successful, the payin will move to the status of Processing.

Separate authorization and capture can be useful for the following payment flows:

- Your merchant is providing the goods or services at a later date. The payment is authorized, confirming the user has the funds for the goods or services, but the payment won't be captured until the goods or services are provided to the user.

- Your merchant needs the ability to authorize an amount that may be greater than the amount that will ultimately be captured. This ensures the user can pay for the total authorized amount, but allows the merchant to capture less, if necessary.

It's important that your merchant's user is informed of the pending payment and when it will be captured, especially if the amount differs between the authorization and capture. Communicating with the merchant's user will reduce inquiries on pending payments and is highly recommended.

Limitations

There are a few limitations to consider with separate authorization and capture:

- An authorized payin can only be captured one time, even if the capture was not for the full authorized amount

- The capture amount must be less than or equal to the authorized amount

- An authorized payin cannot be re-authorized to increase the authorized amount or extend the timeframe to expiration

Authorization expiration

Authorizations expire after a certain number of days, depending on the card brand. Ultimately, it is up to the issuing bank to approve or deny the capture of the authorization if it's passed the expiration date. Rainforest cannot guarantee the capture will be successful if the expiration date has passed. If you capture a payin after the stated expiration date, there can be interchange implications.

Rainforest does not automatically cancel expired authorizations and your platform should:

- Handle the scenario that capturing an expired authorization can result in a Failed payin

- Have a process to cancel authorized payins that have expired

RecommendationIt is highly recommended to capture an Authorized payin within 48 hours of the Authorization.

The following tables explain how long an authorization is valid and when the card brands state the authorizations will expire.

| Card Brand | Expires In |

|---|---|

| Visa | 2 business days |

| Mastercard | 3 business days |

| Discover | 2 business days |

| American Express | 2 business days |

Interchange downgradesIf a payin is captured after the stated expiration date, then there will be interchange downgrades applied by the card brands.

Reports

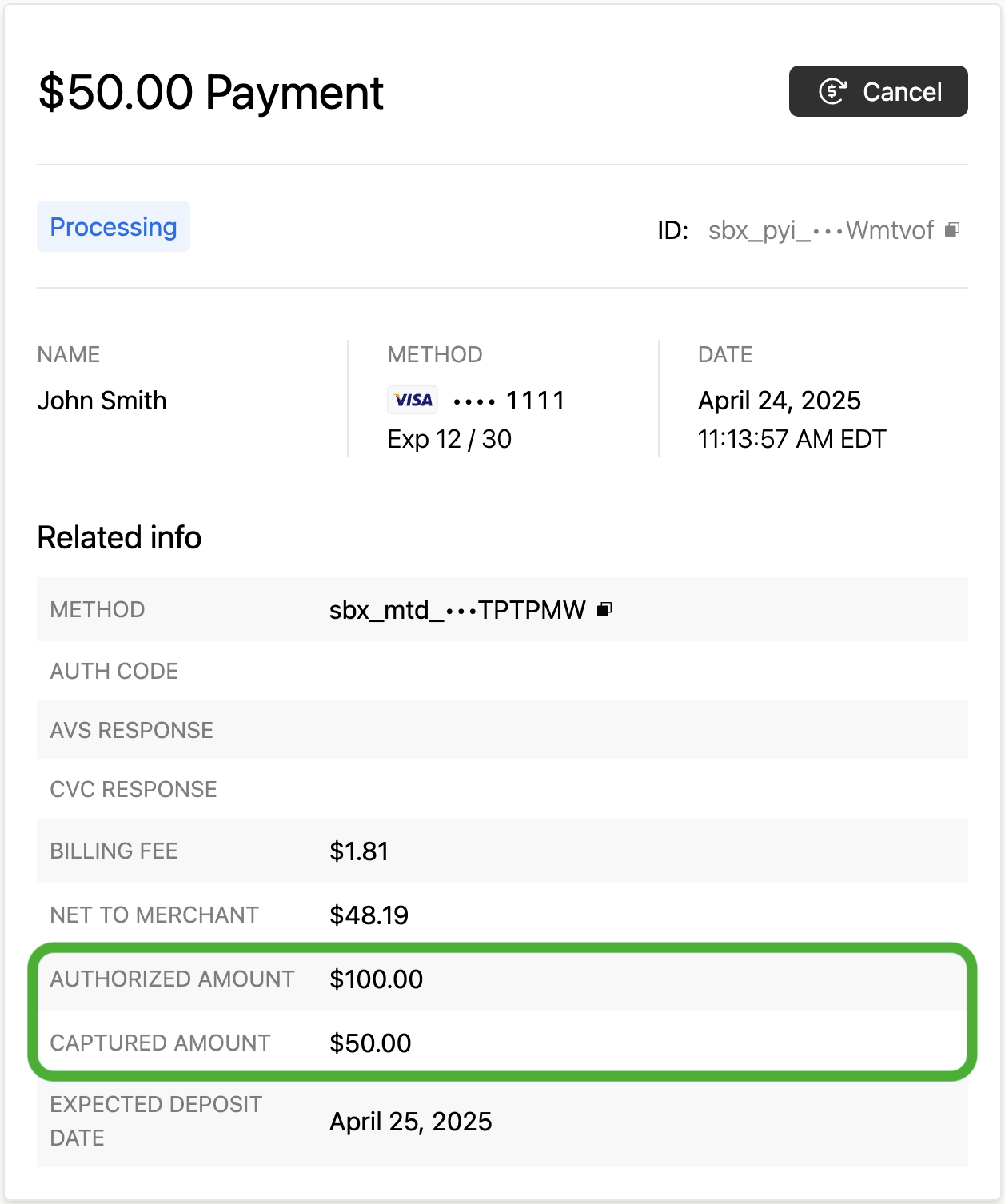

The separate authorization and capture payment flow will return two fields in the Related info section of the Payin Details Component for the authorized amount and the captured amount.

Authorization billing

The separate authorization and capture payment flow does incur additional billing fees.

Authorization fee

The Authorization Fee is billed per authorization attempt, regardless of the outcome of the authorization. Meaning, every authorization attempt that results in a Failed or Authorized payin will incur the authorization fee.

The authorization fee is billed in addition to the per item fee, defined on the merchant billing profile as the Card Payin Rate and Fee. For example, if the payin is processed with the two-step separate authorization and capture flow, then the payin would incur the Authorization Fee when authorized and the payin status moves to Authorized. The Card Payin Rate and Fee will be incurred when the payin is captured and the payin status moves to Processing.

If the payin is processed with the single step authorization and capture flow (i.e. capture immediately), then the payin would only incur the Online Card Payin Rate and Fee when the payin status moves to Processing.

Authorization void fee

The Authorization void fee is billed per voided authorization. Meaning, every payin that is Authorized and then voided before the payin is captured will incur the authorization void fee.

This fee only applies to payins that are in the status of Authorized and then voided. This does not apply to payins that are in the status of Processing and then voided.

Billing merchants

The authorization fee and authorization void fee can be passed onto the merchant via the merchant billing profile.

In the merchant's daily funding deposit, two adjustments will be included for all authorization attempts and all voided authorizations created the day before with an 11pm ET daily cutoff.

For example, the merchant's deposit on August 8, 2024 would include an adjustment for the authorization attempts processed between August 6th 11:00pm ET and August 7th 11:00pm ET.

Updated 9 months ago